What is Open Banking, PSD 2, and the payment initiation service?

April 2021 • 6 min

Open banking is a system that allows sharing financial information necessary for the development of financial products and services. One such product based on open banking is the payment initiation service, which allows customers to pay online in a convenient and fast way– and for merchants to accept such payments without bank-imposed fees. All of this can be done via a third party payment processor, for example, Paysera.

Open Banking vs. PSD 2

In everyday language – these terms are often used as synonyms to explain the process of financial institutions sharing information in order to give consumers more control over their data while also supporting an emerging market of new third party products and services.

But to be precise – PSD 2 is simply a Revised EU Directive on Payment Services. This directive enables services like open banking – secure data sharing among financial institutions through the use of application programming interfaces (APIs). Long story short – PSD 2 is the name of an EU regulation, and open banking is a data sharing service.

When using third party services based on open banking, customers are normally required to consent to such services. It is usually something like simply checking a box on a terms-of-service screen or agreeing to it by continuing the process.

Payment initiation service (PIS) – what is it?

One of the products made possible by open banking is the payment initiation service. It is a service widely used by e-shops and online merchants that grants a licensed third party payment processor with immediate short-term access to the buyer’s account via the online banking in order to initiate the payment on behalf of the buyer.

This service makes it cheaper for the merchant to accept online payments, as well as often faster and simpler for the buyer to make the payment.

Some of the countries where the payment initiation service has completely changed the online shopping experience and is now used widely by many are Lithuania and Latvia. There, online payment processing leader Paysera services around 80 per cent of the existing e-shops and online merchants including the Lithuanian Airports, Elektromarkt, iDeal, and other big names in the local market.

How does the payment initiation service work for buyers?

If an e-shop uses the Paysera payment initiation service to accept online payments – the shopping process is pretty much intuitive for the buyer.

After they are done adding the goods or services to their cart, the buyer proceeds to the checkout. Then – chooses their bank and is taken to the payment window. From here the steps may slightly differ depending on which bank is chosen, but most likely the buyer will be taken to their bank to enter their login details and confirm the payment. Sometimes, the buyer might be able to enter their login details straight in the payment window – skipping the redirection to the bank’s website.

In the future – most online payments will be done this way, since open banking enables information sharing between financial institutions and this allows for a faster and simpler payment confirmation process.

After the payment is confirmed – the buyer is taken back to the e-shop and instantly receives the confirmation email.

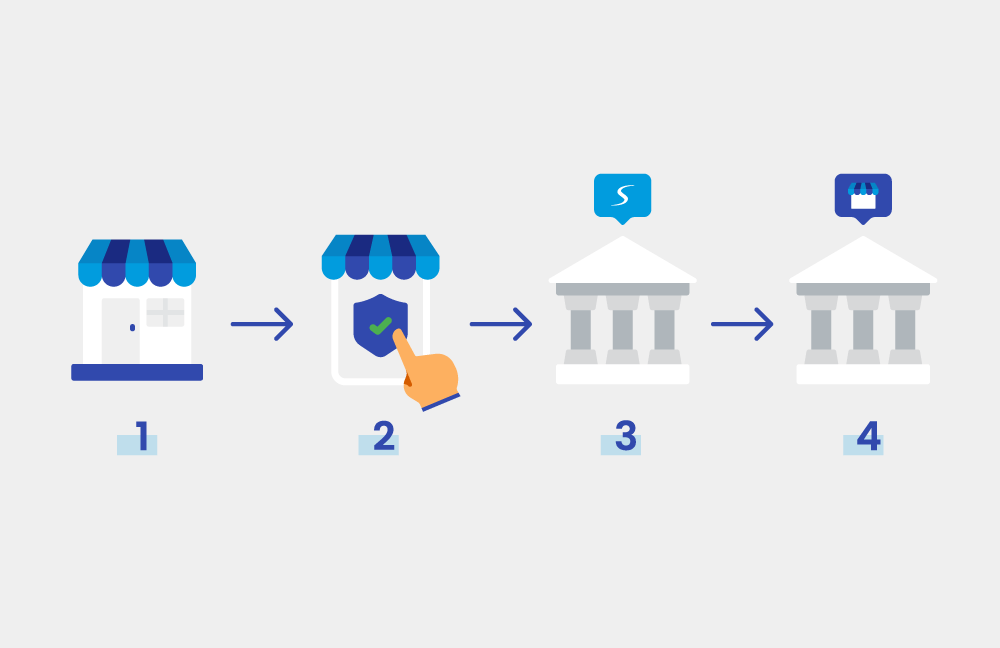

1 – Buyer in the e-shop proceeds to the checkout, chooses their bank, and enters their login details.

2 – Buyer reviews the pre-drafted payment and confirms it.

3 – The payment goes to the Paysera account in the buyer’s bank.

4 – The payment is instantly automatically transferred to the merchant’s Paysera account.

How does the PIS work for an e-shop owner?

In order to start accepting online payments in their e-shop via the Paysera PIS, merchants would need to open a free Paysera account and complete the identification. If the merchant is going to accept payments for a company – they should also open a business account . And yes, the PIS can be also used by merchants that are doing business as individuals and don’t have a business account.

Then, the merchant would need to order a payment gateway service in the Paysera online banking system and create a payment gateway project. It is actually very quick and can all be set up in less than a day. If needed – Paysera has 24/7 client support in English or free consultations available in many different languages during working hours – and all of this can be done together with guidance from the client support team to speed up the process and get all questions answered instantly.

Want to start accepting payments in your e-shop but don’t know where to start? Contact us

Alongside the creation of the payment gateway project – the merchant should download (if needed) a plugin to display all the possible payment methods in the e-shop to the customers. This can also be done via the API integration, however, plugins are available for many different platforms which makes it much easier to complete the integration.

After this is done – you will be able to choose to use the PIS to process payments in the project settings in your Paysera online banking account.

Is the Payment Initiation System and Open Banking secure?

The payment initiation service, just like other services based on open banking, are totally safe and provided only by licensed and regulated service providers. Paysera is a licensed e-money institution with the right to execute activities related to the issuance of e-money and provision of payment services all around the European Union.

Although Paysera is now a global company, it was launched in Lithuania, and so it is periodically checked and audited by the Bank of Lithuania, which ensures the transparency and impeccable activity of Paysera.

The Paysera PIS works in compliance with all the necessary security measures, encrypting the client data, ensuring secure connections to the system, thoroughly identifying clients, including e-shops that use Paysera for payment processing, etc. When clients pay via their online banking in an e-shop that uses the Paysera PIS – extra security is also provided by the buyer’s bank.

Why use the PIS to accept online payments?

There are many reasons to start using the payment initiation service to accept online payments. Some of the most often quoted ones by the e-shop owners that use it: saving money and offering clients to pay in a convenient and secure way via their banks (including Swedbank, SEB, ING Bank, Revolut. See all – Payment Methods > Show.) without the need to sign separate contracts with all the different banks. It is all in one place – the Paysera plugin.

Another reason to use the Paysera PIS is the constant support that e-shop owners can receive from Paysera consultants. We have already onboarded thousands of e-shops in various countries and can answer even the most complex questions regarding online payment processing.

This service will unavoidably roll out across Europe and beyond and is already changing the shopping practices in countries where cash on delivery is still a common payment method. Therefore it is very important not to be left behind and upgrade your e-shop before it is too late.

Have any questions about the payment initiation service? CONTACT US.